Is It A Good Idea to Get A Credit Card?

I once asked myself the same question, “Is it a good idea to get a credit card?” My old self would always say NO. But now that I got a better understanding about the perks and downsides of using a credit card, I am already able to say YES to it.

So is it really a good idea to get yourself a credit card? I have two answers to that. YES, if you have the financial discipline. NO, if it only means being heavily in debt.

And here’s everything you need to know about credit cards.

Getting a credit card is one of the things you should consider if you want to get ahead financially.

I myself once hated the thought of being in debt. But as I opened myself with the idea of maximizing the use of credit cards, I then realized it was one of the best financial decisions I made.

Having a credit card helped me leverage my finances. I mostly use it for cashless transactions, contingencies, and even for some of my investments.

Being a credit cardholder, however, is a huge responsibility. It encourages you to spend an amount that you don’t have — giving you more chance to overspend.

In this article, I will highlight the important things you should know before getting a credit card. Make sure to read this whole thing if you’re interested in having one.

Do I need a Credit Card?

Credit cards are for rich people only. This has always been my mentality before getting myself a credit card. I’m pretty sure we share the same sentiment at some point.

But right now, it becomes easier to acquire one. Some banks even deliver it to your doorstep without any notice.

Still, a credit card is just a fancy term for “soon-to-be-indebt”.

You may splurge yourself with unmindful purchases. And the next thing you know, you’re slapped with the mindblowing figures on your billing statement.

Until you end up living in a monthly rat race just to payoff such horrific amount.

Well, I don’t mean to scare you but that’s one reality of possessing a credit card. The good news is this isn’t always the case.

You can consider this piece of rectangular plastic as a double-edged sword. It can be leverage or enemy — depending on how you use it.

But do you really need it?

If your current financial state is healthy, you might need it — but not necessarily.

If you have existing debts or you usually find it hard controlling unnecessary purchases, then a credit card may not be for you.

What is a Credit Card?

A credit card allows you to borrow an amount instantly. You can use it for almost all types of purchases. Groceries, appliances, gadgets, and even for online subscriptions as long as your merchant accepts credit card payments.

Using your credit card, however, may come with a cost. It can be in forms of annual fee, late payment fee, finance charge, or transaction fees. The good news is you can also benefit from the credit card rewards.

Before getting yourself one, you should be aware of the advantages and disadvantages of using a credit card.

Credit Card Advantages and Disadvantages

Advantages of having a credit card

- If you fully pay your dues on time, you won’t be charged with any finance charges.

- It can save you in times of emergency.

- You don’t have to bring cash.

- More purchasing options, both online and offline.

- Earn rewards and promos for purchasing products or services.

- Quickly grab travel promo opportunities.

Disadvantages of using a credit card

- The fees and interest rates can be costly.

- High probability of fraud and phishing.

- Spend the money that you haven’t earned yet.

- It encourages you to spend more than what you can afford.

- The terms and agreements can be confusing.

- Late payment and over-credit limit penalties can be very scarrrry!

What is the difference between debit card and credit card?

Both debit and credit cards have similar physical features. These are pieces of rectangular plastics containing your name, card number, validity date, and CVV.

The very difference between these two, however, are their contents.

Debit Card

This is mostly known as a savings account card. It is “What you deposit is what you get” card. Whenever you withdraw or purchase using a debit card, it will automatically be deducted from what your account has.

Credit Card

As I said earlier, using a credit card means spending an amount you don’t have. With a credit card, you’re borrowing money to be repaid later.

Take note, however, that there’s a maximum amount of using your credit card. This is what we call the credit limit. Should you spend more than your credit limit amount, you will be charged with an over-limit fee.

Is it better to have a credit card or debit card?

I personally think a debit card is necessary. Where else would you safely put your savings?

A credit card, on the other hand, is something I do not recommend for everyone. If you have a bad credit history, having a credit card will only amplify your bad credit behavior.

But if you know how to use a credit card to your advantage like dodging the finance charges by paying your dues on time, then you can use it to leverage your finances.

Still, between the two, I’d say a debit card is still a better choice. It encourages you to save money and to spend with what you currently have.

What can you do with a credit card?

Here are the most common things you can do with a credit card:

- Buy gadgets or appliances through installment with zero interest

- Purchase goods and services and enjoy cashback rewards

- Shop online

- Pay for online subscriptions like Spotify and Netflix

- Book stays, travels, and car rentals online

- Pay dine outs at restaurants and enjoy cashback bonuses

Important Credit Card Terms you should know:

Credit limit

The maximum amount you can use for purchasing. If you go beyond this limit, you will be charged with an overlimit fee.

Billing cycle

A period of which your credit card bill is generated. It usually runs for one month or 25-31 days.

Billing cycle payment due date

A specific date in which you are obliged to pay for your credit card billing dues. It is usually 18-21 days after the end of your billing cycle.

Statement of Account (SOA)

This is a detailed summary of all the financial transactions you made in a specific billing cycle. This is delivered to you after the end of every billing cycle.

How does a credit card work?

You can think of a credit card as a short-term loan. Basically, the bank as your credit card issuer is the one who pays your purchases in real-time. The purchases you made in a certain period are then billed to you later.

You can swipe your credit card to pay for physical purchases like groceries. You can also enter your credit card details when purchasing online.

But to put everything simply, using a credit card means spending the money you don’t have.

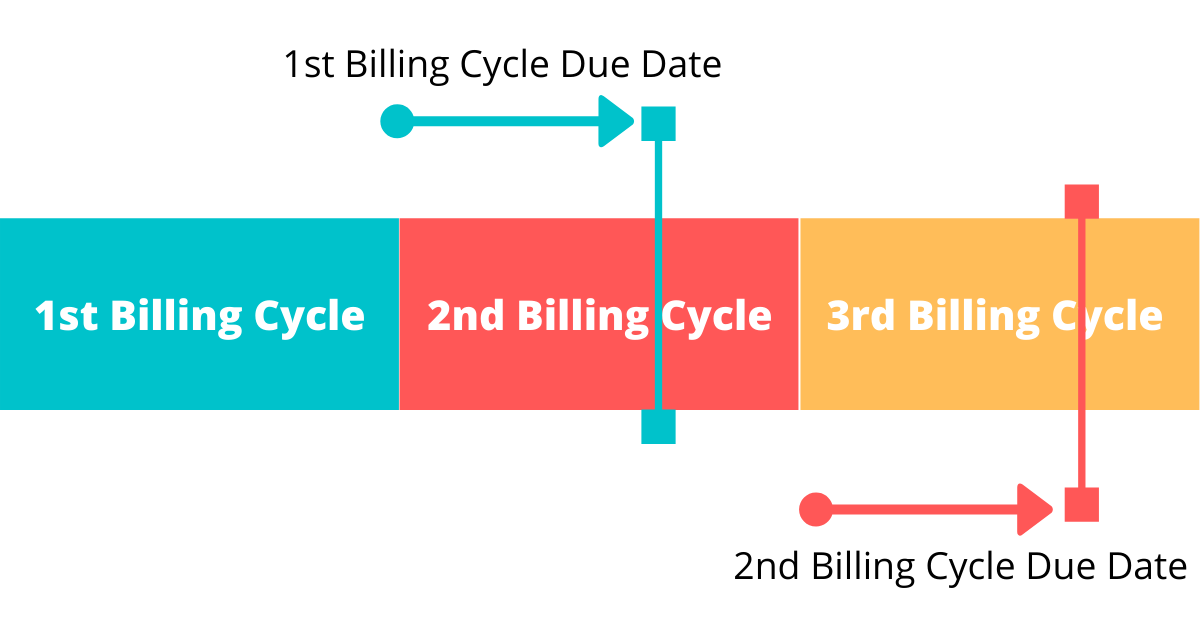

Basically, all the purchases you made in a certain billing cycle are due 18-21 days later. The days between the end of your billing cycle and your payment due date is considered a grace period.

To give you an illustration, this is how it works:

If you made a purchase beyond your current billing cycle period, it will be included for the next cycle’s billing. The color schemes of the figure above speak a lot about it.

Obviously, I can only put limited figures on the image above. But generally, it is just like a loop. So the third cycle’s payment due date is within the fourth billing cycle, and so on.

Now, if you FULLY pay your dues on or before the payment due date, you will not be charged with any finance charges. It’s just like taking a loan and paying it without any interest at all. Yeah, this is what I love about credit cards.

What is a credit card cash advance and how does it work?

A credit card can be used to purchase goods and services both online and offline, but it can also be used for a cash advance. Cash advance is like withdrawing cold cash from an ATM machine.

Cash advance, however, incurs higher interest rates than normal credit card purchasing.

Purchasing products will have an approximate interest rate of 3% per month. But cash advance can go as high as 4-5% per month with an additional cash advance fee of around 600 Pesos or 3% of the cash amount availed, whichever is higher. But of course, it will still depend on the credit card that you are using. In my case, I am using a Metrobank credit card.

How can I see my credit card statement?

Your Statement of Account (SOA) or credit card statement will be delivered to your doorstep every after your billing cycle.

Some credit card issuers, however, are already skipping the physical deliveries of SOA. Instead, they will send you an electronic copy to your preferred email address. This is encrypted with a password. By default, you can open it with your birthday.

What shows up on a credit card statement?

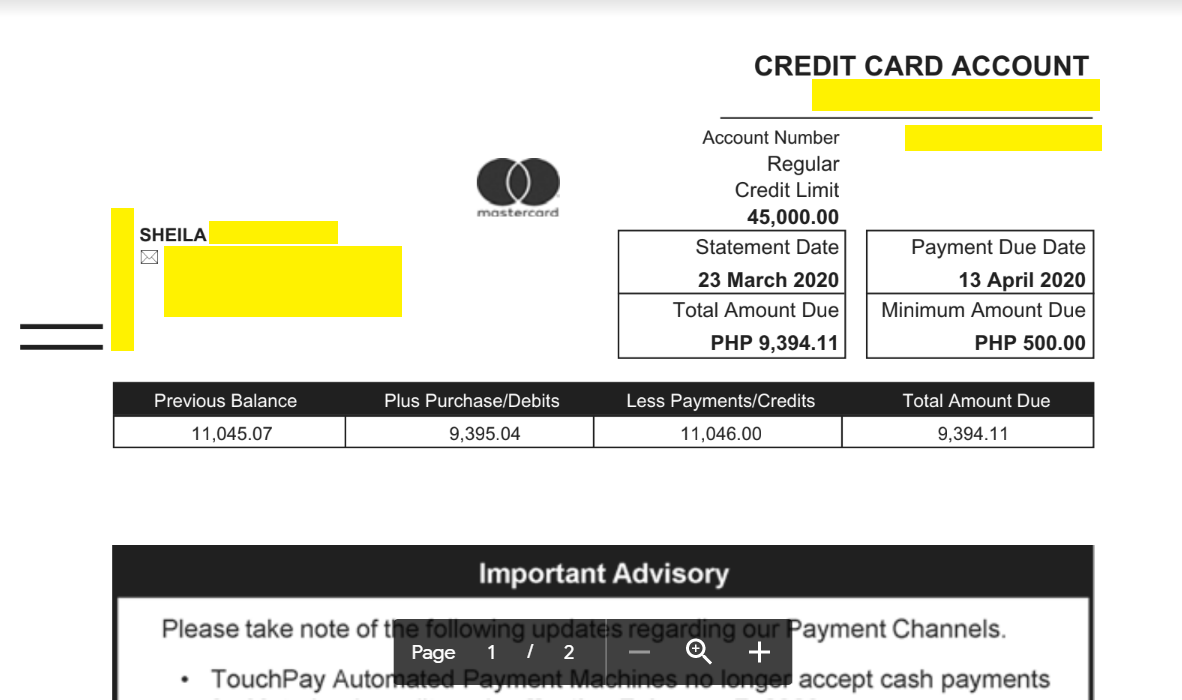

This is an example of a SOA:

Notice the following important details:

- Credit Card Account Number – This is the card number. This is the information I need when paying for my dues.

- Credit Limit – The maximum amount I can borrow. It’s like an XP that replenishes every time I pay. If I purchase beyond this amount, I will be charged with an overlimit fee.

- Minimum Amount Due – The minimum amount I should pay to save myself from other charges.

- Statement Date – The date I received the SOA. Usually at the end of every billing cycle.

- Payment Due Date – I should pay my dues on or before this date. If I pay beyond this date, I will be charged with a late payment fee.

- Previous Balance – My total dues from the previous billing period.

- Plus Purchase/ Debits – The total amount of purchases I made for this current billing cycle.

- Less Payments/ Credits – The amount I paid for the previous billing.

- Total Amount Due – (Previous billing balance + current billing dues – payments made)

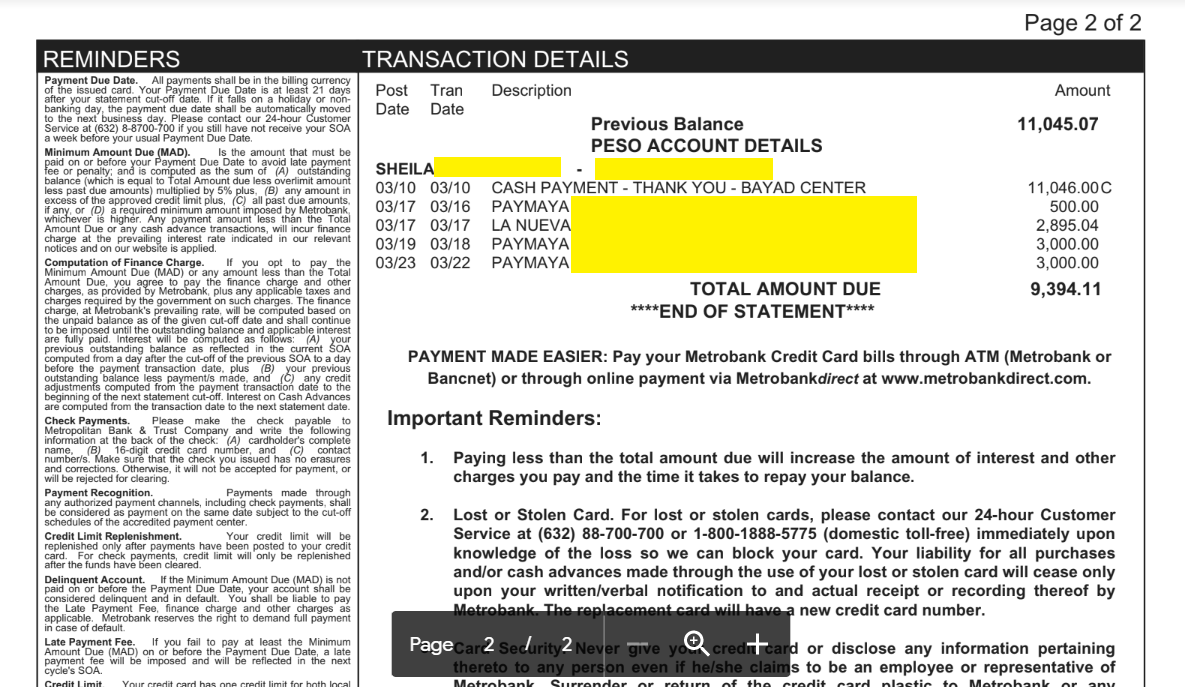

How do I check my credit card transactions?

All your credit card transactions are usually shown on the second page of your credit card billing statement.

This includes your purchases, payments made, and finance charges and penalties (if there’s any).

Credit Card Terms and Conditions Example

I don’t own this section. Still, you might get an idea from this as credit cards usually have the same terms and conditions but differ in fees and interest rates.

I couldn’t stress this enough but before activating your credit card, you SHOULD read its terms and conditions. You’ll usually receive its physical copy along with the card.

In case you lost it, it is still stipulated on your credit card billing statement, usually on the second page.

Here’s an example of the credit card terms and conditions from Metrobank Philippines:

All payments shall be in the billing currency of the issued card. Your Payment Due Date is at least 21 days after your statement cut-off date.

If it falls on a holiday or non-banking day, the payment due date shall be automatically moved to the next business day.

Is the amount that must be paid on or before your Payment Due Date to avoid late payment fee or penalty;

And is computed as the sum of (A) outstanding balance (which is equal to Total Amount due less overlimit amount less past due amounts) multiplied by 5% plus, (B) any amount in excess of the approved credit limit plus, (C) all past due amounts, if any, or (D) a required minimum amount imposed by Metrobank, whichever is higher.

Any payment amount less than the Total Amount Due or any cash advance transactions, will incur finance charge at the prevailing interest rate indicated in our relevant notices and on our website is applied.

If you opt to pay the Minimum Amount Due (MAD) or any amount less than the Total Amount Due, you agree to pay the finance charge and other charges, as provided by Metrobank, plus any applicable taxes and charges required by the government on such charges.

The finance charge, at Metrobank’s prevailing rate, will be computed based on the unpaid balance as of the given cut-off date and shall continue to be imposed until the outstanding balance and applicable interest are fully paid.

Interest will be computed as follows: (A) your previous outstanding balance as reflected in the current SOA computed from a day after the cut-off of the previous SOA to a day before the payment transaction date, plus (B) your previous outstanding balance less payment/s made, and (C) any credit adjustments computed from the payment transaction date to the beginning of the next statement cut-off.

Interest on Cash Advances are computed from the transaction date to the next statement date.

Please make the check payable to Metropolitan Bank & Trust Company and write the following information at the back of the check: (A) cardholder’s complete name, (B) 16-digit credit card number, and (C) contact number/s.

Make sure that the check you issued has no erasures and corrections. Otherwise, it will not be accepted for payment, or will be rejected for clearing.

Payments made through any authorized payment channels, including check payments, shall be considered as payment on the same date subject to the cut-off schedules of the accredited payment center.

Your credit limit will be replenished only after payments have been posted to your credit card.

For check payments, credit limit will only be replenished after the funds have been cleared.

If the Minimum Amount Due (MAD) is not paid on or before the Payment Due Date, your account shall be considered delinquent and in default.

You shall be liable to pay the Late Payment Fee, finance charge and other charges as applicable. Metrobank reserves the right to demand full payment in case of default.

If you fail to pay at least the Minimum Amount Due (MAD) on or before the Payment Due Date, a late payment fee will be imposed and will be reflected in the next cycle’s SOA.

Your credit card has one credit limit for both local and international purchases. The cash advance and installment facilities form part of your total credit limit.

Moreover, the credit limit assigned to the principal card member is shared with all supplementary card members. The total credit limit is subject to security and credit limit management conditions that Metrobank may impose for your benefit.

Metrobank reserves the right to decline or approve any transaction and/or suspend the credit card privileges of the principal card member and his/her supplementary card members without prior notice if the credit limit will be or has been exceeded.

Metrobank may demand immediate payment of the amount over the credit limit or the total amount outstanding. An over credit limit fee of PHP750 or such other amount as Metrobank may set is charged for every overlimit occurrence.

All charges, advances, or amounts in currencies other than Philippine Peso (PHP) shall be converted to PHP.

Transactions in US Dollar, Hong Kong Dollar, Japanese Yen, Euro, Singapore Dollar, Australian Dollar, British Pound, Canadian Dollar, Chinese Yuan, Swiss Francs and Danish Kroner shall be converted using the foreign exchange selling rate of Metropolitan Bank and Trust Company on transaction posting date.

Transactions denominated in currencies other than the aforementioned will be converted using the foreign exchange buying/selling rate of Mastercard and Visa on transaction posting date. The billing currency amount represents the amount due to Metrobank for its purchase and payment on the Card Member’s behalf of the foreign currency necessary to discharge the amount(s) due to Mastercard/Visa or the acquiring bank and/or foreign merchant affiliates.

The said transactions may also be subject to additional fees to cover assessment fee that may be charged.

These additional fees shall likewise apply to transactions involving foreign currencies converted to Philippine Peso at point of sale whether executed in the Philippines or abroad or online.

A flat fee of Php600 or 3% of the cash amount availed, whichever is higher, is charged on the date the cash advance is taken.

An additional PHP500 will be charged if transacted over-the-counter.

Finance charges for cash advances at the prevailing interest rate of 3.75% per month shall accrue from the date the cash advance is taken and will continue until the cash advance is completely settled.

A 5% service fee will be levied on gaming transactions charged to your credit card.

Gaming Transactions include those that involve the placement of a wager, purchase of lottery tickets, in-flight commerce gaming, and the purchase of chips or other values in conjunction with gaming activities provided by establishments such as casinos, race tracks, airlines, and the like.

A reprinting fee of P100 will be charged per request for reprinting and delivery of your monthly Statement.

Disregard this if you opted for mSOA or electronic SOA.

A processing fee of P250 will be charged for every approved Cash2Go, Balance Conversion, or Balance Transfer transaction.

A fee of PHP1,500 will be charged for check payments which were returned due to reasons such as, but not limited to, insufficient funds, unsecured deposit, stop payment order or closed account.

Overpayments shall not earn interest and shall be applied to succeeding credit card usages and charges.

In case of overpayments on closed accounts, a monthly account maintenance fee, or amount equivalent to the credit balance, whichever is lower will be charged to accounts with credit balance that are closed or with no activity for the past 12 months.

Please notify us within thirty (30) days from statement date of any erroneous billing. Otherwise, the SOA will be considered correct. Likewise, any payment shall be taken as conclusive proof of your concurrence.

Visit https://metrobankcard.com/cards/compare-all to see the complete Table of Fees and Charges.

What happens if you never pay your credit card?

Now, if you’re unable to pay your credit card bill in full on time, you can opt to pay for the minimum due. Take note, however, that your remaining balance will reflect again on your next credit card billing, with incurred finance charge or interest rate.

But if you have no plans of ticking off that credit, expect to pay for late payment fees and receive increased interest rates. Worse, it could damage your credit score.

If you continue to miss your payments, your card could be frozen. More than that, you can be sued legally.

But you can talk to your credit card issuer to give you some options at the very least.

I know a friend who skipped her credit card dues for years. She just ignored the bank notices until legal action was initiated against her. It was then that she talked with her bank and was given another chance to pay it off in a specific period of time.

My Personal Experience with Credit Cards

I was once on the “I hate credit cards. I will never try to get myself one” side, because why not? We all heard credit card stories of being heavily in debt.

But after weighing things out, I finally decided to have one.

I often use it for online transactions and recurring bill payments. Sometimes, I also use it to fund my online investments.

But I always make sure to only spend an amount I know I can FULLY pay on or before the payment due date.

I always pay my credit card dues in FULL and on time to save myself from finance charges and late payment fees. It’s like having a loan without paying any interest. Again and again, that’s what I love about credit cards.

As of this moment, I currently have two credit cards. I dedicate one for physical purchases while the other for online transactions so I can closely keep track of my spendings.

If you’re from the Philippines, I highly recommend the Citibank Citi Simplicity Credit Card for its topnotch online app integration and fast delivery of SOA. It also charges NO ANNUAL FEE. Forever. You also check this comprehensive guide from Grit.ph on how to get a credit card in the Philippines.

Important Credit Card Reminders

1. Make sure to fully understand how the credit card works. Read the terms and conditions before activating your account.

2. If you pay less than your total amount due, your balance may be subjected to higher interest rates.

3. If you lose or had your credit card stolen, contact your bank issuer immediately to block incoming transactions. You will then be given a new credit card of the same account but with a different credit card number.

4. Never share your personal information like OTP and CVV. Credit card issuers will NEVER ask it from you.

5. Make sure to update your account for any changes like address and contact number.

So is it good to have a credit card?

I personally consider having a credit card a wise financial decision – only if you are disciplined enough to manage your dues on time. You can use it to leverage your financial life.

In fact, if your credit histories prove how good of a payor you are, it will be easier for you to easily apply for bank loans. This is how essential credit cards are to build your credit score.

If you are not so sure though, just spare yourself. Never get yourself something that will just push you to incur greater debts. Perhaps it would just be better to follow Dora and say “Swiper, no swiping!”.

Sheila

Sheila is a civil engineer by profession but has switched careers to become a copywriter. She loves making sales through stories that are relatable to the average person. She's also a sucker for memes and thinks she’s the funniest person in the world (even though she knows that’s not true). Her favorite drink is Kopiko Brown coffee, but she'll also take tea or beer if it's offered.

5 Comments

Pingback:

Pingback:

Sir

Good day. I just want to ask a question related to credit card.

Let’s just say I have a relative that gone rogue and maxed out their credit card, and they never paid it. When I apply for credit card, will my application be affected when they found out I’m related to them?

Hopefully you can reply to my question.

Sheila

Hi Serjay,

Apparently, credit card companies will only care about your own credit history, so it is unlikely that a relative’s bad credit history will affect yours.

Pingback: